Global Broker Regulation Inquiry App

About WikiFX

English

简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

اردو

Global markets continue to reach record highs on hopes of an end to the Middle East conflict

Abstract:Key TakeawaysU.S. stock markets reached fresh all-time highs, led by strong AI momentum and continued demand for semiconductor companies.The Nasdaq 100 broke above the 30,000 level for the first time

Key Takeaways

U.S. stock markets reached fresh all-time highs, led by strong AI momentum and continued demand for semiconductor companies.

The Nasdaq 100 broke above the 30,000 level for the first time in history as tech stocks dominated global markets.

Micron Technology and SK hynix both surpassed the historic $1 trillion market capitalization milestone during the week.

Oil prices plunged nearly 10% after optimism surrounding potential U.S.-Iran negotiations reduced supply disruption fears.

Bitcoin came under strong selling pressure and dropped toward the $73,000 region as inflation concerns weighed on risk sentiment.

Stronger-than-expected U.S. PCE inflation data reinforced expectations that the Federal Reserve may keep interest rates elevated for longer.

Global Stocks Advance Higher, US Indices at Record Highs

Next Week Forecast

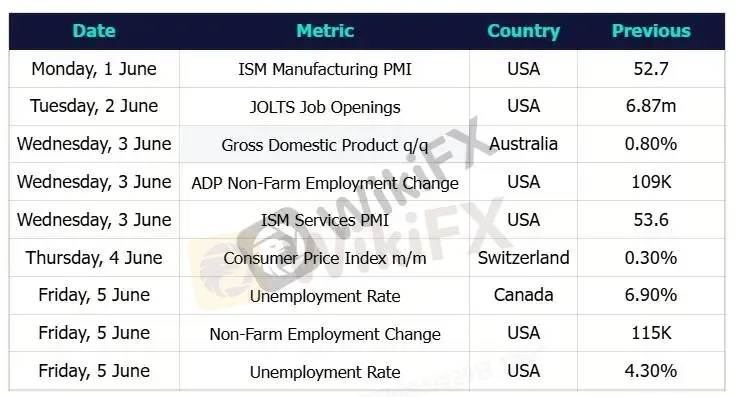

Major Economic Calendar Events for the Upcoming Week

Global financial markets experienced another volatile week as investors navigated record highs in U.S. equities, a sharp collapse in oil prices, renewed pressure on Bitcoin, and critical inflation data from the United States. Market sentiment shifted several times throughout the week, initially driven by geopolitical tensions in the Middle East before optimism surrounding potential negotiations between the United States and Iran pushed energy prices sharply lower and supported risk appetite across global equities.

U.S. stock indices continued their impressive rally, with major benchmarks reaching fresh all-time highs during the week. The Dow Jones Industrial Average opened the week near 50,784 and climbed to a new historical high around 51,129 before giving back part of its gains and eventually closing near its weekly opening levels. Despite the late pullback, the Dow remained supported by strong corporate earnings and continued optimism surrounding the resilience of the U.S. economy.

The Nasdaq 100 remained the strongest-performing major index globally as investor demand for artificial intelligence and semiconductor-related stocks accelerated further. The index opened the week near 29,651 and managed to break above the psychological 30,000 level for the first time in history, ending the week above 30,200. Semiconductor giants continued leading the rally, with both Micron Technology and SK hynix reaching the historic $1 trillion market capitalization milestone during the week. Investors continued pouring capital into AI-related companies amid expectations that global demand for data centers, AI chips, and memory products will remain extremely strong over the coming years.

Asian equity markets followed the positive momentum from Wall Street. Japan‘s Nikkei 225 remained near multi-decade highs as weakness in the Japanese Yen continued supporting export-oriented companies and technology shares. South Korea’s KOSPI index outperformed several regional peers after strong gains in semiconductor stocks boosted the overall market. Investors continued focusing heavily on the AI sector, particularly after the strong performance of memory chip manufacturers throughout the week.

One of the most important events of the week was the release of the U.S. Personal Consumption Expenditures (PCE) inflation report, which is considered the Federal Reserves preferred inflation gauge. Headline PCE inflation rose to 3.8% year-over-year, while Core PCE increased to 3.3% year-over-year. Monthly Core PCE also came in stronger than expected, reinforcing concerns that inflation in the United States may remain elevated for longer than markets initially anticipated. Following the data release, Treasury yields moved higher while expectations for aggressive Federal Reserve rate cuts later this year declined.

Looking ahead to next week, investors are expected to focus heavily on labor market data, Federal Reserve commentary, and ongoing geopolitical developments. U.S. equity markets may continue attempting to push toward new record highs if AI-related momentum remains strong and bond yields stabilize. However, markets remain vulnerable to additional inflation surprises or any hawkish signals from Federal Reserve officials.

Oil prices are likely to remain highly sensitive to developments surrounding negotiations between the United States and Iran. Continued diplomatic progress could keep pressure on crude prices, while any unexpected escalation in geopolitical tensions may quickly reverse the recent decline.

Gold is expected to remain volatile as traders continue reacting to inflation expectations, Treasury yields, and geopolitical uncertainty. As long as prices remain above key support levels, buyers may attempt another move toward recent highs.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

XTB Exposure Report 2026: Mounting KYC & Fund Withdrawal Complaints

WikiFX

WikiFXBONUS Review 2025: Is This Forex Broker Safe?

WikiFXTrading.com Secures MiCA Licence in Cyprus as Crypto Access Becomes Part of Its EU Strategy

WikiFXHow Outcome Bias Tricks Beginners into Copying the Wrong Trades

WikiFXFBS Review 2026: Complaints, Withdrawals, and Risk Signals

WikiFXLive from Wealth Expo Colombia 2026: WikiFX Strengthens Growing Partnerships Across LATAM

WikiFXDeriv Review 2025: Is This Forex Broker Safe?

WikiFXBrokers With Maximum Credible Regulatory Licences

WikiFXManual vs. Mechanical Trading: Turning Market Feel Into Automated Rules on MT5

WikiFXUITFX Review 2026: Unregulated Status and Withdrawal Warnings

WikiFXCurrency Calculator

USD

CNY

Current Rate:0

Enter amount

USD

Redeemable Amount

CNY

Calculate